You’ve done everything right. You’ve built a successful business—let’s say an online piano lesson platform—with happy clients and steady monthly revenue. You need a R50,000 loan to run a big marketing campaign. You walk into your traditional bank, and the manager asks for three years of audited financials, a detailed business plan, and what physical collateral you can put up.

Your “assets” are your website, your good name, and your client list. The bank manager doesn’t understand. You get rejected.

Does this sound familiar? This exact scenario is why fintech (financial technology) and alternative lenders are booming in South Africa. They’ve built an entirely new system for a new kind of economy—one built on data, speed, and digital businesses just like yours.

What Are Alternative & Fintech Lenders?

This term covers any lender that isn’t a traditional, “big four” bank. They are tech companies first and finance companies second.

There are two main types you’ll encounter:

-

Specialist Online Lenders: These are companies (like Lulalend, Retail Capital, etc.) whose entire business is to offer fast, short-term business funding online. They are not banks.

-

Digital & Neo-Banks: These are new, app-based banks (like TymeBank or Capitec’s business arm) that have built their SME lending from the ground up using technology, making it faster and more integrated than their older competitors.

They all share one common goal: to use technology to say “yes” to good businesses that the old system overlooks.

The Big Difference: Why They’re Winning

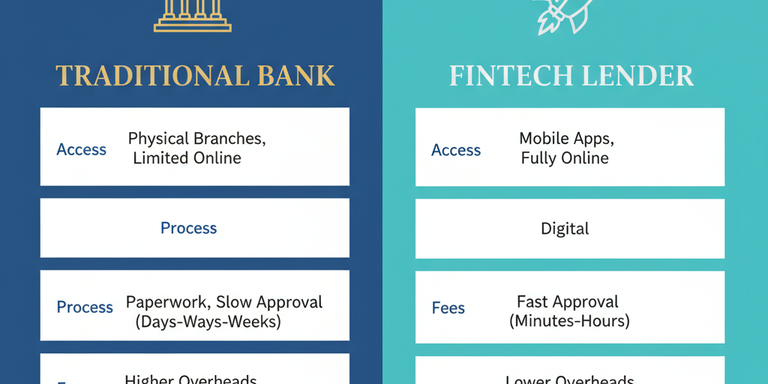

The core difference isn’t the money; it’s the process, speed, and requirements. A traditional bank’s process is built on paper, history, and physical assets. A fintech’s process is built on data, speed, and digital performance.

Why Is This Happening Now in South Africa?

This isn’t a small trend; it’s a major shift in the market, driven by four key factors:

-

The SME “Funding Gap”: For years, traditional banks have focused on large corporate clients and personal loans. They’ve found it too costly and difficult to underwrite small businesses needing R50,000 or R100,000. Fintech lenders have built technology to specifically target this massive, underserved market.

-

High Mobile & Internet Penetration: South Africa has the digital infrastructure. Business owners are online, comfortable with apps, and ready to manage their finances from their phones.

-

Inflexible Bank Models: Traditional banks love collateral (like a house or car). This is a non-starter for “asset-light” businesses—like online consultants, e-commerce stores, or your digital piano school.

-

New Data Sources: The rise of e-commerce (Shopify), digital payments (Yoco, PayFast), and online accounting (Xero) has created a “digital footprint” for every business. Fintechs can read this footprint; banks often can’t.

The Pros of Using a Fintech Lender

This new model provides powerful advantages, especially for modern SMEs.

-

Access: This is the #1 benefit. They fund businesses that banks ignore: newer businesses (6-12+ months old), e-commerce stores, and “asset-light” digital businesses.

-

Speed: Because their decision-making is automated, they can offer “instant funding” in as little as 24-48 hours, not weeks.

-

Data-Driven Decisions: They use new technology, as detailed in our guide to AI-Driven & Alternative Credit Scoring. They’ll analyse your real-time bank account or sales data, not an old credit report.

-

Flexible Products: They offer innovative products that match your cash flow, like a Merchant Cash Advance (MCA) (where you repay with a percentage of your daily sales) or a revolving Line of Credit.

The Risks: What to Watch Out For

This new world isn’t without its risks. You must go in with your eyes open.

-

The Cost of Convenience: This is the most important trade-off. Alternatively, unsecured, 24-hour loans are more expensive than a traditional bank loan. Always check the total cost, not just the monthly payment.

-

The “Wild West” Factor: The space is newer and less regulated than the established banks. It’s crucial to stick with reputable lenders and avoid “guaranteed approval” loan sharks.

-

Confusing Terms: You’ll see “Factor Rates” instead of “Interest Rates (APR).” These can be very misleading and hide a much higher cost.

Who Wins? You Do.

The rise of fintech lenders doesn’t mean traditional banks are obsolete. It means that for the first time, South African SMEs have choice.

-

Go to a Traditional Bank when: You need a large, long-term loan (like a commercial mortgage) and you have significant assets and a long trading history.

-

Go to a Fintech Lender when: You need short-term working capital fast, you have strong digital sales or cash flow, and your business doesn’t fit the old, rigid “collateral” model.

As a modern business owner, your most valuable asset is your data. Find a lender who knows how to read it.