Short-term business loans can seem like a quick and easy solution for cash flow gaps or unexpected expenses. In South Africa, a variety of lenders, from traditional banks to fintech companies, offer these products with promises of fast approval and minimal paperwork. However, beneath the surface of seemingly low-interest rates and quick turnaround times lies a complex web of hidden costs that can dramatically increase the total cost of borrowing. For small and medium-sized enterprises (SMEs), failing to understand these nuances can lead to a debt spiral that hinders, rather than helps, business growth.

This article, which is intended to be a resource for financial education, will delve into the various fees associated with short-term business loans in South Africa and provide a practical guide on how to calculate the true cost of your loan.

Understanding the Components of a Loan’s Cost

When you get a loan, the sticker price—the interest rate—is only one piece of the puzzle. The total cost of borrowing is the sum of all charges over the life of the loan. In South Africa, these costs are typically made up of a few key components:

Stop guessing. Start building.

We've built a free Business Idea Generator Tool that walks you through this exact framework and generates a professional Validation Report.

Access the Free Tool-

Interest Rate: This is the most obvious cost. It’s the percentage charged on the principal amount of the loan. Short-term loans often have higher annual percentage rates (APRs) than long-term loans due to the increased risk for the lender. While some may be fixed, others may be linked to the prime lending rate.

-

Initiation Fee: This is a one-time fee charged by the lender for processing your loan application and setting up the account. This fee is often capitalised, meaning it’s added to your total loan amount and paid off over the loan term.

-

Monthly Service/Admin Fees: Many lenders charge a recurring monthly fee for the administration of the loan account. While these fees may seem small individually, they add up significantly over the loan term.

-

Early Settlement Penalties: While many fintech lenders in South Africa may offer discounts for early settlement, some traditional lenders still charge a penalty if you repay your loan before the agreed-upon term. This is a crucial factor to consider if you anticipate an early windfall of cash.

-

Credit Life Insurance: This is an insurance premium that covers the outstanding debt in the event of the borrower’s death, disability, or retrenchment. This is a legally required component for many loans and is charged monthly.

-

Missed or Late Payment Fees: A late or missed payment can trigger a penalty fee, which can further compound your debt.

How to Calculate the Total Cost of Borrowing

To get a clear picture of what you’ll pay, you need to go beyond the advertised interest rate and calculate the Annual Percentage Rate (APR). The APR includes the interest rate plus any additional fees, giving you a more accurate representation of the cost.

Here’s a simple formula to calculate the total cost of borrowing:

Total Cost of Borrowing = (Total Repayments) – (Original Loan Amount)

To break it down further, you can use this more detailed calculation:

Total Cost of Borrowing = (Principal Amount x Interest Rate) + (Initiation Fee) + (Monthly Service Fee x Number of Months) + Other Fees

Free Tools Mentioned

Access our interactive calculators to simulate your specific business numbers.

Unlock All Tools FreeLet’s look at a representative example in the South African context:

-

Loan Amount: R100,000

-

Loan Term: 12 months

-

Interest Rate: 25%

-

Initiation Fee: R1,200

-

Monthly Service Fee: R69

In this scenario, a quick calculation will show that the total interest paid is R25,000. But if you include the fees, the total cost of borrowing becomes much higher.

Calculation:

-

Initial Interest: R100,000 x 0.25 = R25,000

-

Total Monthly Fees: R69 x 12 months = R828

-

Total Repayments: (R100,000 + R25,000) + R1,200 + R828 = R127,028

While the interest rate may seem manageable on its own, the fees add another layer of expense, pushing the true cost of the loan higher than you might have initially assumed. This is why it’s vital to request a full repayment schedule from any prospective lender.

Mitigating the Risks and Finding Alternatives

Before you sign on the dotted line, consider these proactive steps:

-

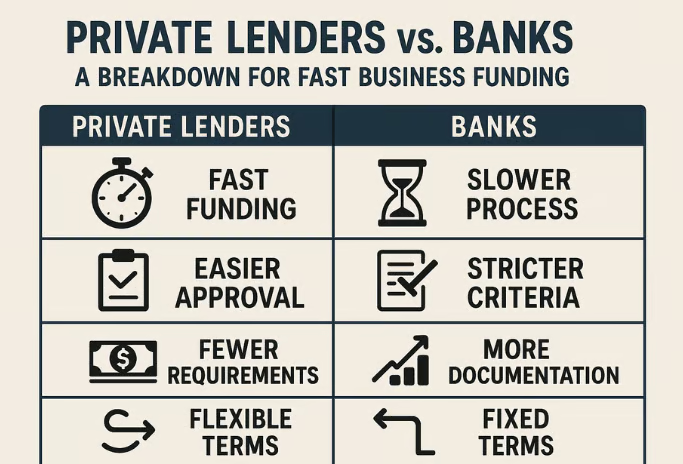

Shop Around: Don’t settle for the first offer. Compare interest rates, fees, and repayment terms from multiple lenders, including both traditional banks and alternative lenders that may be more flexible. For a detailed guide on this, you can read our article on how to choose the right business loan for your SME.

-

Read the Fine Print: Carefully examine the loan agreement for any hidden clauses or fees. If you don’t understand something, ask for clarification. The NCR (National Credit Regulator) in South Africa provides guidelines for fair lending practices.

-

Consider Alternatives: Short-term loans are not the only option. Explore other forms of financing, such as invoice factoring (selling your invoices for immediate cash), revolving credit facilities, or even government grants for small businesses. For more information on these, check out our guide on alternative funding options for small businesses in South Africa.

While short-term business loans can be a lifesaver for South African SMEs, they are often a costly solution. By taking the time to understand all the potential fees and accurately calculate the total cost of borrowing, you can make a more informed decision and ensure your financial health remains on a stable footing.

Need Startup Capital?

If your business is already trading, check your eligibility for up to R5M in unsecured funding.

Check Eligibility